If you're researching crypto-backed loans, Nebeus and Ledn are two platforms you're likely to encounter. Both allow you to borrow against your crypto without selling it. Choosing between them is about which one matches your situation.

This guide compares both platforms across the dimensions that actually matter for crypto borrowers: supported assets, loan structures, LTV ratios, how you access your funds once borrowed, and regulation. The goal is to give you the clearest possible picture so you can make an informed decision.

Nebeus and Ledn at a Glance

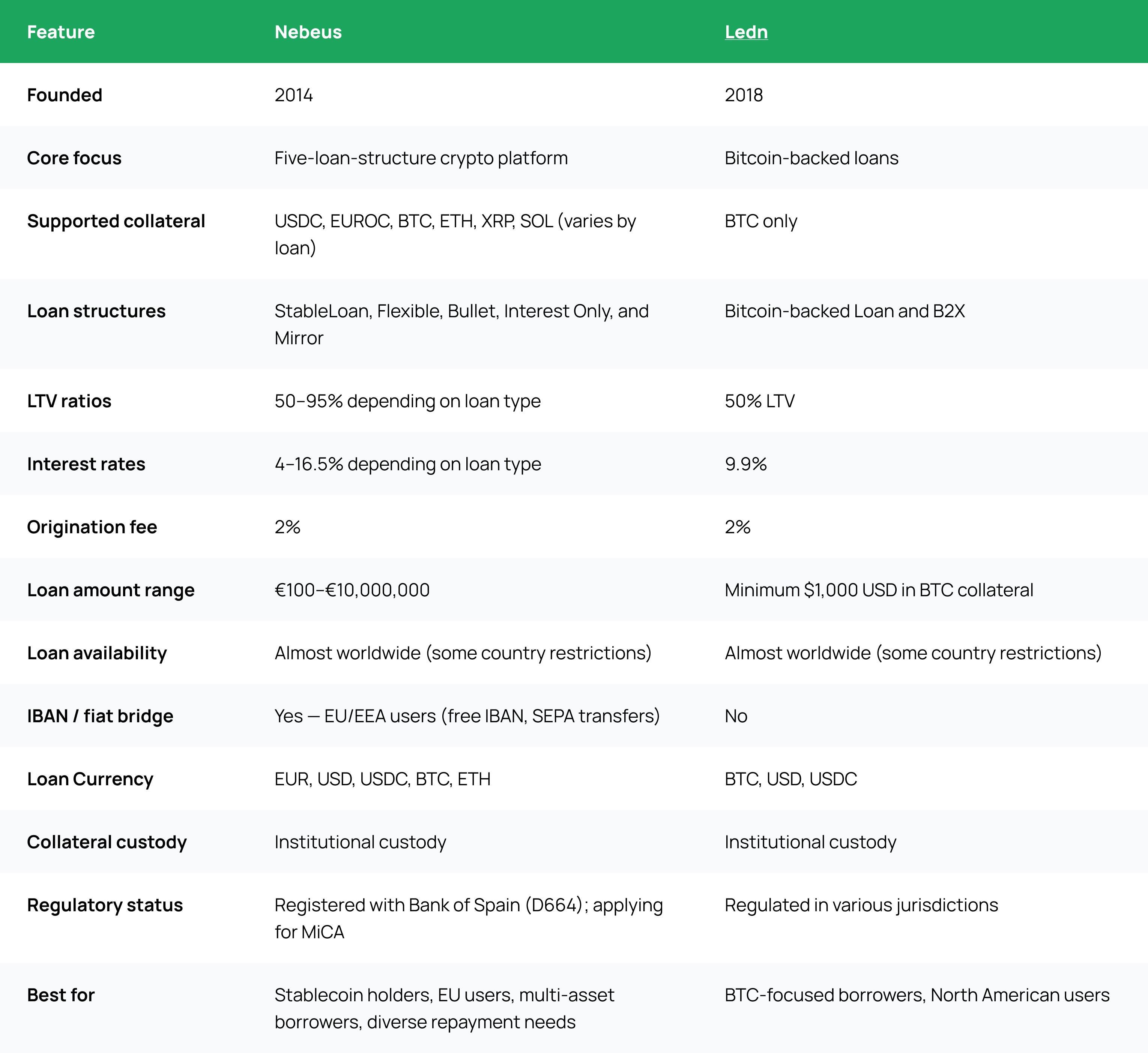

Ledn launched in 2018 with a focused mission: help Bitcoin holders access liquidity without selling their BTC. It offers two loan products: a Bitcoin-backed Loan for straightforward BTC liquidity, and B2X — a service that combines a loan with a BTC purchase to double a user's Bitcoin position. It built a reputation in the crypto lending space through a commitment to transparency — including pioneering Proof of Reserves audits, a genuinely meaningful step for an industry that has often struggled with trust. For straightforward Bitcoin-backed borrowing, particularly for users based in North America, Ledn has a solid track record.

Nebeus has been operating since 2014, making it one of the oldest crypto lending platforms in the world. Rather than building around a single asset or loan type, it operates as a crypto-fintech platform with five distinct loan structures — each designed for a specific borrower profile — and a native European IBAN that connects crypto liquidity to everyday spending. Collateral is safeguarded by BitGo, one of the world's largest digital asset custodians with $64 billion in assets under custody, and insured by a $250 million policy underwritten by a syndicate of Lloyd's of London insurers.

Nebeus vs Ledn: The Key Differences

Loan Products: One Strategy or Five?

The most substantive difference between these two platforms is the loan architecture.

Ledn's model is built around Bitcoin.

- Bitcoin-backed Loan: deposit BTC as collateral, borrow in USD or USDC, repay at the end of the 12-month term or early with no penalty — no monthly payments required.

- B2X: combines a loan with a BTC purchase to double a user's Bitcoin holdings. When the loan is repaid, both the collateral and the newly purchased BTC are returned to you.

Both products operate at a fixed 50% LTV and a 9.9% annual interest rate, with a minimum of $1,000 USD equivalent in BTC collateral.

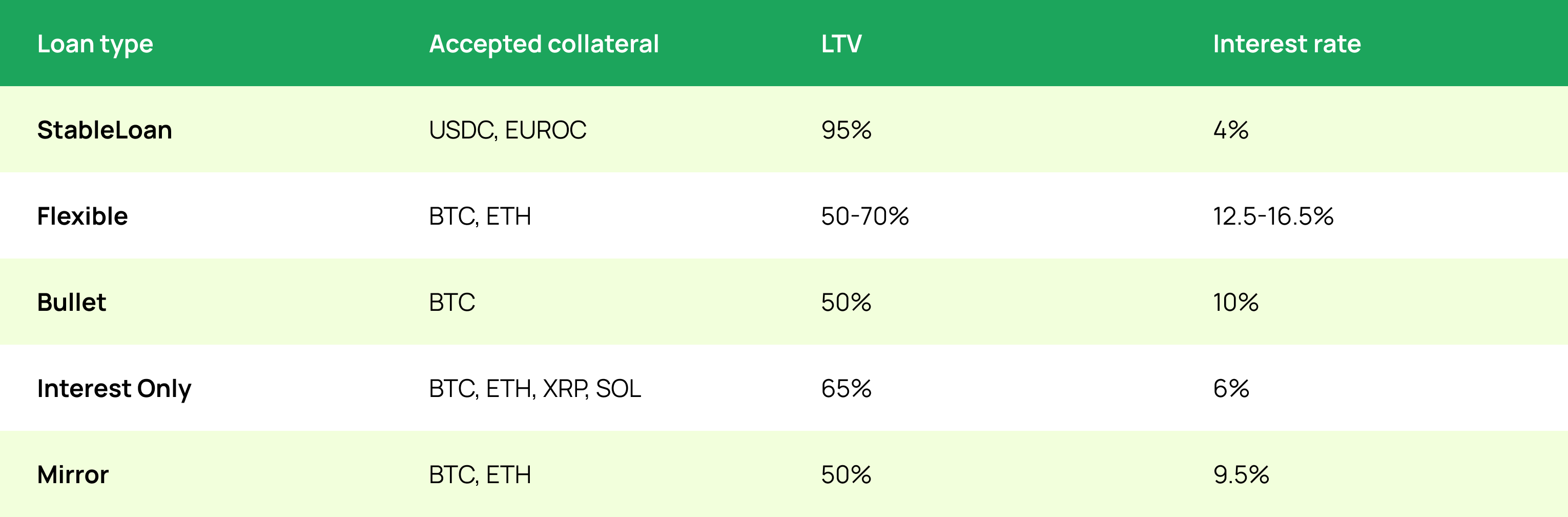

Nebeus structures its loan offering around five distinct loan types.

- StableLoan is built for users holding stablecoins — specifically USDC or EURC. With a fixed 95% LTV and a 4% interest rate, it's designed around the mechanics of stablecoin collateral, which doesn't carry the price volatility of BTC or ETH. For someone holding stablecoins who wants to access EUR liquidity without triggering a taxable disposal event. Loan terms run from one day to 18 months, with monthly interest repayments and a 2% origination fee.

- Flexible Loan accepts BTC or ETH as collateral and operates with LTVs ranging from 50% to 70% and interest rates from 12.5% to 16.5%, depending on the specific terms. Repayment is monthly, covering both interest and a portion of the principal — similar to a standard loan amortisation structure, but with more customisation options. Loan terms run from one day to 36 months.

- Bullet Loan accepts BTC as collateral at a fixed 50% LTV and a 10% interest rate. No monthly repayments — the entire principal plus interest is settled in a single payment at the end of the loan term. Terms run from 29 days to 18 months. This structure suits borrowers who expect a predictable liquidity event (a salary, a bonus, an asset sale) and want to align their repayment accordingly.

- Interest Only Loan accepts the broadest collateral base of any Nebeus loan: BTC, ETH, XRP, and SOL. LTV is fixed at 65%, with a 6% interest rate. Monthly payments cover interest only; the principal is settled at the end. With terms running up to 48 months — the longest available — it's suited to borrowers who want to minimize monthly outgoings while maintaining crypto exposure over a longer horizon.

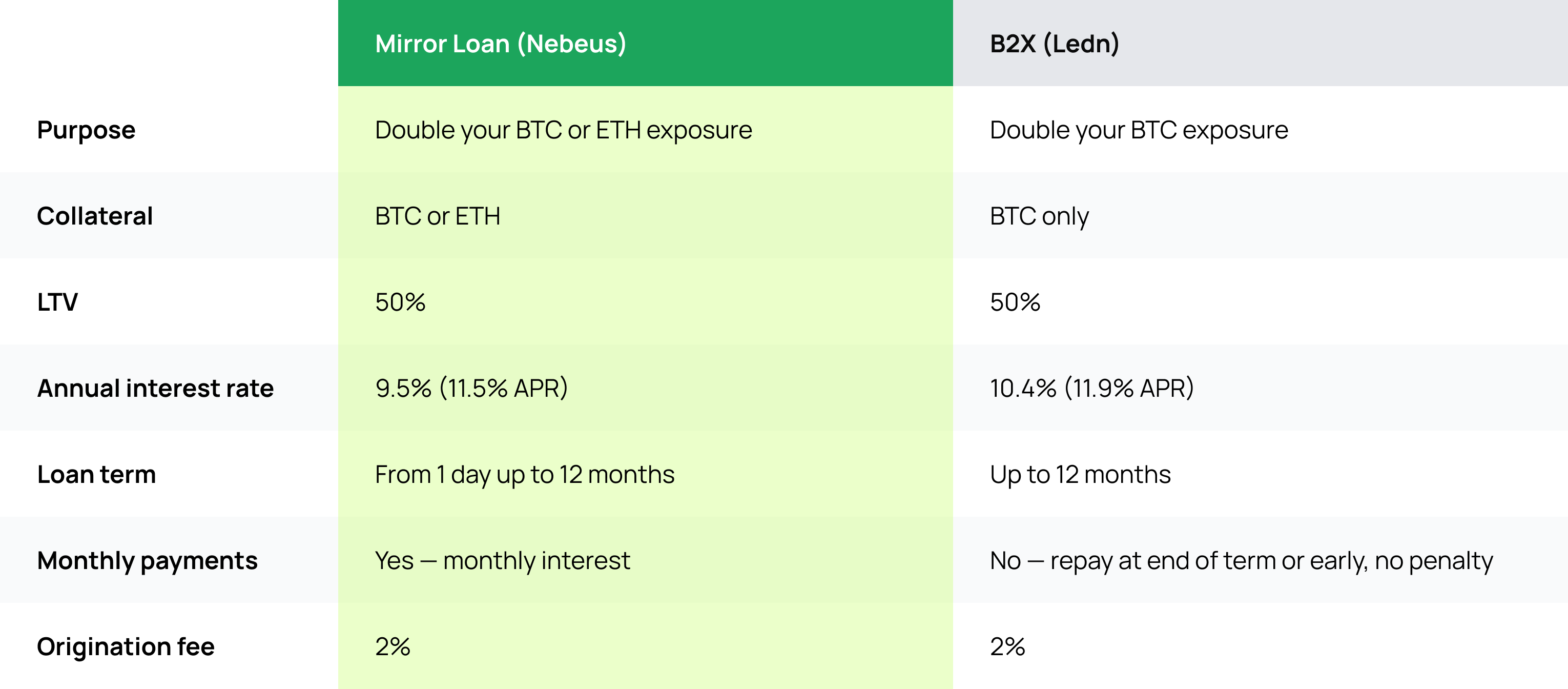

- Mirror Loan accepts BTC or ETH and operates at a fixed 50% LTV with a 9.5% interest rate and terms of up to 12 months. The mechanism is specific: Nebeus matches a BTC deposit with an equivalent amount of BTC, using both as collateral to double the depositor's position. It's positioned explicitly at sophisticated investors who understand the mechanics and the downside.

Mirror Loan vs B2X: 2 Ways to Increase Your Crypto Exposure

Both Nebeus and Ledn offer a leveraged exposure product — Mirror Loan and B2X respectively. They share the same core purpose: use your existing crypto holdings as collateral to increase your position in a crypto asset without deploying new capital. Where they differ is cost and flexibility.

Supported Assets and LTV Ratios

The asset question is foundational — it determines whether you can use a platform at all, and how much liquidity you can access from what you hold.

Ledn’s Bitcoin-backed Loan is built exclusively around Bitcoin collateral, at a fixed 50% LTV. That means for every €10,000 worth of Bitcoin deposited as collateral, you can access approximately €5,000 in liquidity. The conservative LTV reflects the price volatility inherent in BTC; a meaningful buffer between collateral value and loan value reduces the risk of liquidation in a downturn.

The picture changes significantly when the collateral is a stablecoin. Because stablecoins are, by design, pegged to a stable value, the price volatility risk that justifies conservative LTV ratios on BTC loans doesn't apply in the same way. Nebeus's StableLoan reflects this: 95% LTV on USDC or EUROC collateral, at a 4% interest rate. On €10,000 in stablecoin collateral, that's the difference between accessing €5,000 (at a 50% LTV) and accessing €9,500.

For users holding assets beyond BTC — ETH, XRP, SOL, or stablecoins — the collateral flexibility question becomes the central filter.

Here's how Nebeus's loan types break down:

Best for BTC-only collateral: Ledn's focused model is well-suited for users whose holdings are concentrated in Bitcoin and who want a straightforward loan experience.

Best for diversified multi-asset portfolios: Nebeus’ ability to use BTC, ETH, XRP, SOL, USDC, or EURC — across different loan structures — offers flexibility that a single-collateral platform can't match.

Getting Your Loan Into the Real World

Receiving a loan is one thing. Being able to use it for the everyday expenses that prompted the borrowing in the first place is another.

Once a crypto-backed loan is approved on Nebeus, the funds are credited to the user's Nebeus wallet in fiat (e.g., EUR). For EU and EEA users, the wallet connects directly to a free personal IBAN account — from which funds can be transferred via SEPA to any bank account, used for bill payments, or moved internationally, typically within seconds. The IBAN is free to obtain and activate through the app. The flow is: loan approved → funds in Nebeus wallet → IBAN transfer → real-world spending.

Ledn does not offer an IBAN or direct European fiat integration. Funds from a Ledn loan would require an additional step to reach a traditional bank account — through a separate exchange, bank transfer, or third-party service which could mean a potential block coming from a crypto source. For users with established fiat infrastructure, this may be a manageable inconvenience. For users who want to manage crypto and everyday money from a single platform, it's a meaningful gap.

This matters most for expats, digital nomads, and international workers in Europe — a group for whom access to a straightforward, crypto-compatible IBAN is often more practically significant than it might appear on paper. Being able to pay rent, cover bills, and make transfers directly from the same account where loan funds land changes the day-to-day experience considerably.

Regulation, Security, and Transparency

Trust is non-negotiable in crypto lending, and both platforms have made meaningful commitments to establishing it — through different means.

Ledn's Proof of Reserves programme is a genuine industry contribution. They were among the first crypto lending platforms to commission independent audits verifying that customer assets are backed 1:1 by real holdings. For users whose primary concern is verifying that their collateral actually exists where it's supposed to, this is a serious and credible answer. Ledn also has an operational track record dating to 2018.

Nebeus has operated since 2014 — making it one of the oldest crypto apps of its kind. Collateral deposited on Nebeus is held in custody by BitGo as one of its main partners and one of the largest institutional custodians in the world with $64 billion in assets under custody. That collateral is covered by a $250 million insurance policy underwritten by a syndicate of Lloyd's of London insurers — a level of coverage that goes beyond what many platforms in the space offer. Nebeus is registered with the Bank of Spain under registration number D664 for digital asset custody, purchase, and sale services.

It's important to be precise about what the Bank of Spain registration covers: it applies to those specific services — digital asset custody, and purchase and sale. It does not mean that Nebeus's loans or verification processes are supervised or approved by the Bank of Spain.

Neither platform is a bank. Neither offers deposit insurance or government-backed capital protection. These are digital asset platforms operating within the regulatory frameworks applicable to their respective services and jurisdictions.

Geographic Availability: What You Actually Get Access To

Geography shapes the practical experience on both platforms more than most comparisons acknowledge.

Nebeus offers crypto-backed loans worldwide — subject to specific country restrictions, which are worth verifying for your jurisdiction before applying. The IBAN, however, is exclusively available to EU and EEA users. This means the full product suite — loan → Nebeus wallet → IBAN → SEPA spending — is the experience for European users. Users outside Europe can access loans and use the Nebeus wallet, but the fiat bridge via IBAN doesn't apply.

Ledn's geographic availability is concentrated primarily in North America and selected other markets. European availability has expanded, but the absence of IBAN or SEPA integration means European users face additional steps to connect a Ledn loan to everyday European banking.

For users in Europe, the geographic fit is an important filter before anything else. For users in North America, the calculus is different — Ledn's established track record and BTC focus may be the more relevant starting point.

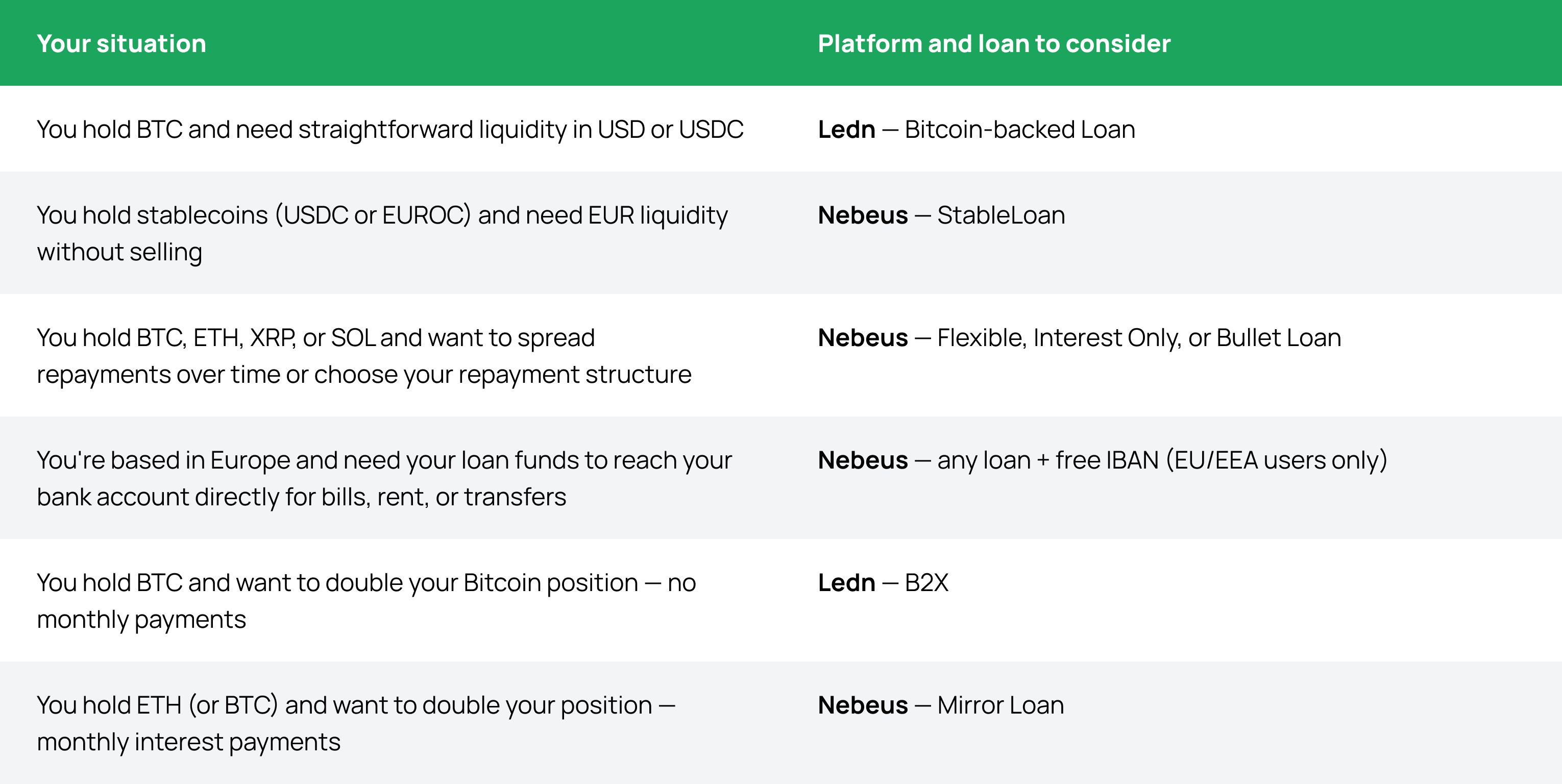

Which Platform Fits Your Profile?

There's no universally correct answer here — but there is a right answer for your specific situation. The table below maps common borrower profiles to the platform most likely to serve them well.

Explore Nebeus loans or start your application to see which loan structure fits your situation.

Frequently Asked Questions

Is Nebeus or Ledn better for crypto-backed loans? Neither platform is universally better — they serve different user profiles. Ledn is well-suited for BTC-focused borrowers, particularly those based in North America, who want a straightforward lending product with a strong Proof of Reserves track record. Nebeus is better suited for users holding stablecoins or diversified portfolios, European users who need IBAN integration, and borrowers who need a specific repayment structure. The right choice depends on your asset base, geography, and borrowing purpose.

Does Ledn have an IBAN? No. Ledn does not offer an IBAN account or native European SEPA integration. Users receiving a loan through Ledn would need to transfer funds to a traditional bank account through a separate off-ramp process.

Which platform offers more collateral options? Ledn's two loan products — the Bitcoin-backed Loan and B2X — both accept BTC only. Nebeus accepts six assets across its five loan types: USDC, EUROC, BTC, ETH, XRP, and SOL. For borrowers whose holdings extend beyond Bitcoin, collateral flexibility is the central filter.

Which platform is better for short-term borrowing? Nebeus's loan terms start from one day across most of its products, including StableLoan, Flexible, and Mirror Loan — making it compatible with short-term liquidity needs. Ledn's Bitcoin-backed Loan and B2X are both structured around a 12-month term, though early repayment is available with no penalty. If your borrowing horizon is days or weeks rather than months, Nebeus offers more structural flexibility.

Does Ledn accept stablecoins as collateral? No. Both Ledn loan products — the Bitcoin-backed Loan and B2X — require BTC as collateral..

What is the difference between Nebeus Mirror Loan and Ledn B2X? Both products are designed to double your crypto exposure using your existing holdings as collateral. The main differences: B2X is BTC-only and charges 10.4% annual interest with no monthly payments. The Mirror Loan accepts BTC or ETH and charges 14.5% interest with monthly interest payments. Both operate at 50% LTV for up to 12 months and carry significant liquidation risk.

How does Ledn and Nebeus handle margin calls if my collateral value drops? Both platforms monitor collateral value in real time and alert borrowers when LTV approaches the liquidation threshold. Nebeus offers Automatic Margin Call Management — it automatically replenishes collateral from your Nebeus wallet balance without requiring manual action. Ledn offers a similar Auto Top-Up feature that moves available BTC from your Ledn account to top up collateral when LTV hits 70%. In both cases, if no action is taken and collateral isn't topped up, partial liquidation may follow.

){kind=link}